The Future of Cities

How the pandemic is changing the way we live

Our cities have come under intense pressure over the past 12 months, due to the sudden impact of the pandemic, and the immediate shut down of crowded places.

Some have wondered, given how so many have been able to work from home, whether there will be long-term mass migration out of cities to the suburbs.

While employers contemplate working life after lockdown, businesses that rely on busy city centres are also left questioning whether that income will ever return.

Many fund managers do expect changes to take place in cities, but think ultimately they will survive because they offer so much of what people have missed during lockdown.

This report aims to look at some of these issues.

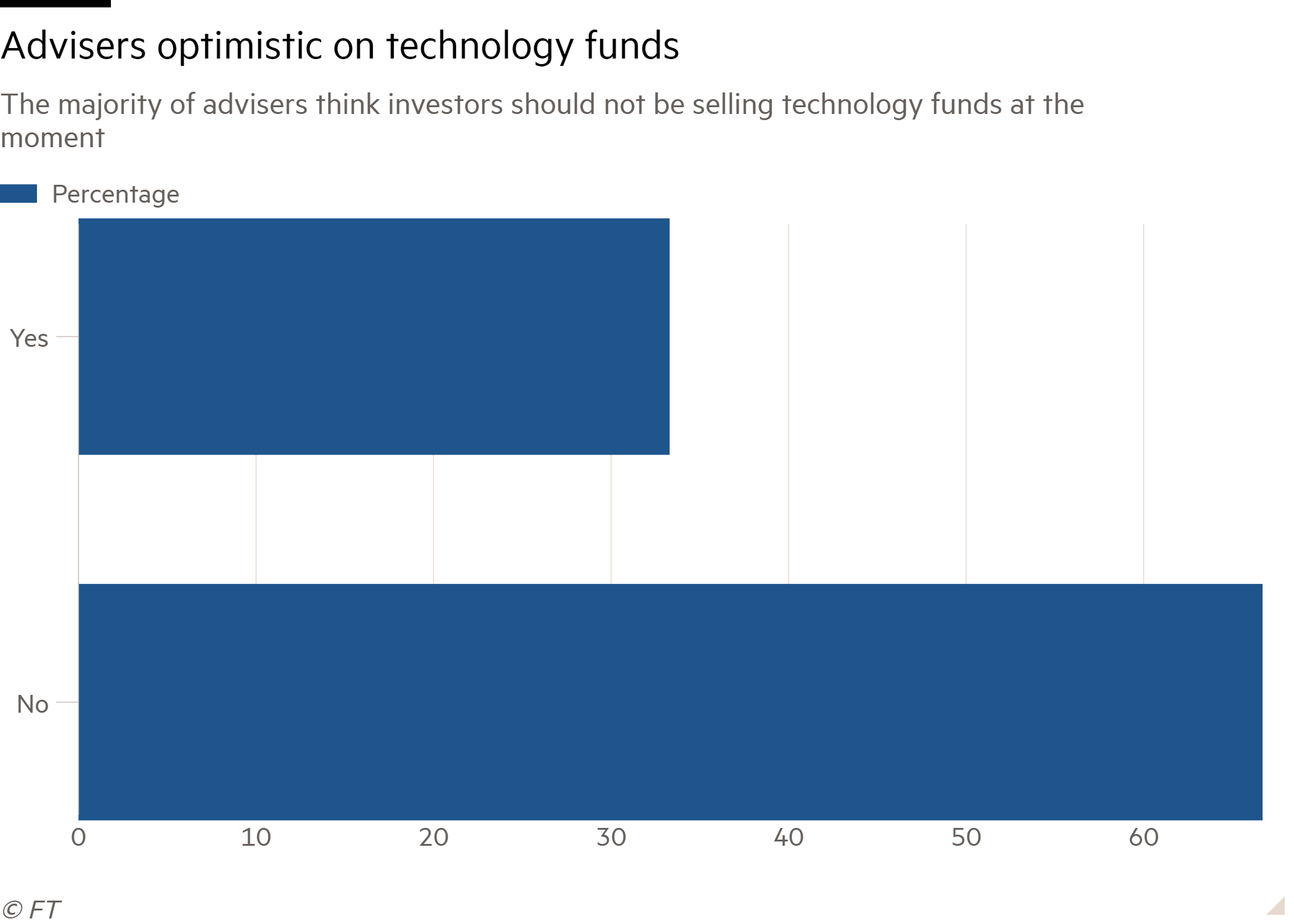

Majority of advisers keep the faith with big technology funds

The rapid sell-off in technology stocks has not changed most advisers' attitude to big technology funds, according to the latest FTAdviser poll.

The poll, which was conducted via Twitter, shows that around two thirds of advisers are optimistic about the outlook for technology funds, with one third believing now is the time to sell.

The question comes amid a steep sell off in the shares of the Scottish Mortgage Investment Trust, the largest trust in the UK market, and a vehicle with heavy exposure to the technology sector in the US and China.

The shares were over £14 in the middle of February, but now are below £12.

The reason for the sell-off is fear amongst market participants that vaccines will prompt a stronger than expected economic recovery, and lead to higher inflation, and the earlier withdrawal of the monetary stimulus put in place by central banks.

This would negatively impact those equities which trade at the highest valuations at this time, including technology stocks.

Technology stocks are also particularly vulnerable to this trend as they mostly do not pay dividends, and as bond yields rise, this means the income being sacrificed by owning non-yielding assets increases.

Investors will be looking closely at long lasting effects of the pandemic

We won’t, says Adrian Lowcock, head of personal investing at the Willis Owen platform, want more Netflix when this is all over.

Lowcock says that whenever lockdowns are lifted and bleary eyed populations begin to emerge into the world, the likelihood is that they will want to do those things forbidden to them over the past year, such as travel, and visit pubs and restaurants, rather than buy more of the products or services they have consumed during lockdowns.

He says this is why the increased optimism around vaccine programmes has translated into a stronger performance for stocks that are more sensitive to economic activity, and relative underperformance for those companies that performed strongly during the pandemic.

But while the public embracing the habits of old amid a burst of economic activity is one of the few certainties investors can find in markets right now, the longer-term picture is more complex, says Ed Smith, head of asset allocation research at Rathbones Unit Trust Management.

Lockdowns have led to the sight of normally crowded city streets being deserted, as a greater portion of economic activity has become digitised, rendering physical location less relevant.

This has had the effect of making the economic downturn that came with the pandemic somewhat less severe than might have been expected.

In the early days of lockdown, in March 2020, Peter Toogood, chief investment officer at Embark Group, described an economy where “GDP has stopped”, as we were not permitted to leave our houses and engage in many forms of activity.

But the activity levels were actually switched online, as people discovered they could easily work from home, and firms discovered that online sales significantly increased to replace the physical sales that were lost.

This meant that rather than activity being confined to a comparatively small corner of the economy, it turned out that far more of the country could operate, and instead it is specific areas of the economy that could not operate.

Bank of England chief economist Andy Haldane outlined the consequences of this change in emphasis recently when he gave a speech outlining how the UK economy is presently operating at much closer to its level of potential now than was the case during the Global Financial Crisis.

He said this is because, during the global financial crisis, many areas of the economy contracted, and there were no areas of the economy where growth expanded, but in the pandemic, while many areas contracted sharply, new types of growth emerged.

For Haldane, this means the prospect for the short and medium term is that the economy will return to operating at its full level of potential more quickly than in 2008, and so inflation will rise sharply.

Smith says the key will be to understand how, as working patterns change, people and companies spend their extra time and income, he believes this question will be key to determining two of the questions that matter most to investors in the years to come, the level of growth in the economy, and the level of inflation.

The inflation question

Smith says that if people begin to work from an office only two or three days a week, this would typically be expected to have a massively disinflationary impact on the economy, with lower inflation keeping bond yields low and boosting the returns for growth stocks over the longer-term.

If people are working from home some of the time, this would also likely mean that city centre focused assets, such as offices, pubs, and shops in prime locations would suffer a decline in demand.

Smith says it may be that the consumption which no longer takes place in city centre locations switches to suburban and rural locations; this means demand or spending falls in prime central areas but the overall level of growth in the economy would remain the same but be less concentrated on cities and spread more evenly around the country. However, if people simply spent less, then the long-term outlook for economies as a whole would be for lower.

Real estate is responsible for 40 per cent of all global emissions

Zsolt Kohalmi, global head of real estate for Pictet Alternative Advisers says: “Sustainability has been an underlying trend that has been greatly accelerated through the pandemic. There is no turning back.

“Real estate is responsible for 40 per cent of all global emissions, and with over 70 per cent of buildings in Europe over 20 years old, improving the environmental footprint of buildings will be one of the key areas of focus for occupiers and investors in the coming years.

“Investors in turn will be pushed by their retail or institutional investors to be more ESG-focused. I expect this to show up in the capital value of a green building being superior to a non-green building at an increasing pace.

“Essentially non-green buildings will be increasingly penalized, a bit like diesel cars have been over the last few years.

“By investing in commercial offices and facilitating a significant transformation – making it more environmentally friendly, facilitating innovation and collaboration, embracing technology – there is the scope to achieve better returns while doing good at the same time.

Fahad Kamal, chief investment officer at Kleinwort Hambros, says the desire shown by many as a result of the pandemic to move out of cities and to the countryside is “a very old one”, and something which he says has always happened, but that city centre economies will always be strong.

He says that while many of the existing uses to which city centre property is put will be redundant, new purposes will be found for those outlets, though unemployment will be higher until that happens, and rents likely will be lower.

Kamal believes it is inevitable that these factors will keep inflation low. He adds that it may be that, whereas in the past, individuals lived in the suburbs and went into the cities for work, in future it may be that people work from the suburbs and travel into city centres at weekends for their leisure time.

But he does not at present find commercial property an attractive asset class, as he believes valuations remain too high to properly reflect the looming changes.

He said these changes could mean people spend a greater portion of their income away from city centres, and as city centres tend to be more expensive than suburbs, this causes disinflation.

Today, around half of us around the world live in cities but by 2050 this proportion is expected to reach as high as 68 per cent

Smith says another factor could be that wages do not rise very much for those who work from home, as employers will be able to avoid pay increases because inflation is lower, and commuting costs are lower.

The technology issue

Peter Michaelis, head of sustainable investments at Liontrust says increased urbanisation has been a major theme in the global economy for many years.

“Today, around half of us (55 per cent) around the world live in cities but by 2050 this proportion is expected to reach as high as 68 per cent.

“This would mean a doubling of the urban environment and equivalent to 70m people moving to cities every year for the next three decades, with close to 90 per cent of this increase taking place in Asia and Africa.”

He says city living as it is currently constituted is significantly bad for the environment, and as governments around the world strive to reduce emissions, he believes cities in the future will have a greater focus on energy efficiency, and will be largely free of cars.

He says cities in future will be largely capable of generating their own energy supply, while social housing will also be a major theme.

Among his holdings is Optivo, a social housing provider which also has a focus on the energy efficiency of its dwellings.

David Harrison, who runs the Rathbones Global Sustainability fund says the cities of the future will have charge points for electric vehicles as a central feature of street corners.

Alex Illingworth, who jointly runs the Artemis Global Select fund and Mid Wynd investment trust, says: “People have been talking about ‘Smart Cities’ for years without making a huge amount of progress. That’s because, unless you’re creating somewhere virtually from scratch, you are lumbered with an existing infrastructure.

Cities are centres for art and culture and the best paid jobs will still be most likely from companies in metropolitan areas

“Cities are difficult things to change. However, the pandemic has opened up the opportunity to think radically, and it’s changed working practices for many people. We don’t think everyone will suddenly be moving from London to the countryside and opting for home working.

“It’s a factor, but it has been overplayed. Cities are centres for art and culture and the best paid jobs will still be most likely from companies in metropolitan areas.

“But a city does have to be somewhere you want to live because many of us have more options. That means cities have to have green spaces. We will see less retail. We may see fewer cafés and restaurants, but we will still need them – the idea that we’re all going to start bringing Tupperware to work sounds implausible.

“And as we’ve learned in lockdown, restaurants are an important part of social life and the culture of the city.”

In terms of what this means for investors he says: “Some of the transformations required will depend on government subsidy, and that always introduces an element of risk. Governments are fickle and you can suddenly find a subsidy removed.

“Sometimes the smartest thing you can do as an investor is identify the companies you should not be investing in – those facing disruption from new technology. When Edison opened his lab in 1879 to demonstrate his new incandescent light bulb and power generator, there were several competing technologies available from scientists like Sawyer, Man and Maxim.

“Edison’s first bulbs had a 15-hour life. His triumph was not a foregone conclusion, but natural gas stocks plummeted on news of his demonstration.

“Our thematic approach to investing and our ESG principles enable us to capture in a lower-risk way the benefits of the trends shaping the modern world. Just as importantly, they help us avoid areas that face a headwind or obsolescence.”

The global equity fund manager Nick Train is another who believes the key to investing in the future is to find those companies that can be resilient in the face of change, rather than trying to identify the winners from the changes before they happen.

While Train and the tech managers are thinking about where our cities will be, the value managers are avoiding those judgements; the question is who will be right in the long term.

Daniel Leal-Oliva/AFP via Getty Images

Daniel Leal-Oliva/AFP via Getty Images

AP Photo/Alberto Pezzali

AP Photo/Alberto Pezzali

Reuters/Temilade Adelaja

Reuters/Temilade Adelaja

Michael Nagle/Bloomberg

Michael Nagle/Bloomberg

What investors can learn from Bill Gates’ climate warning

When one of the world’s wealthiest individuals writes a book on avoiding climate disaster – and suggests changes we all need to make to our lifestyles – it is easy to be cynical.

But the high-profile intervention of Microsoft founder Bill Gates in the climate change debate should be welcomed.

This is not just a highly intelligent wealth creator, but somebody who, arguably, has unique access to information and insight. Furthermore, his Gates Foundation has achieved impressive results in tackling global health and education issues.

He clearly has an appetite for solving the seemingly unsolvable.

His book, How to Avoid a Climate Change Disaster: The Solutions We Have and the Breakthroughs We Need , should be a must read, particularly for those investing in the great energy transition.

He captures the challenge of the century: how do we stop adding of 51 billion tones of greenhouse gases to the atmosphere every year?

This needs to be done as fast as possible to avoid climate disaster and in an economic and balanced way.

As a fund manager who lives and breathes this trend, the solutions identified by Gates affirm the decisions being made by me and my team - the technologies we are backing and the innovations we are identifying.

Gates sets out the need to quickly reduce our reliance on fossil fuels over the next 30 years to get to net zero. Net zero does not necessarily mean that we will not be using fossil fuels any more.

In power generation and in ground transportation, that is a strong possibility, but in other areas, such as steel and cement manufacturing, or fertilisers or even lightweight plastics, we will likely still be using some fossil fuels.

Carbon, however, will need to be captured rather than released into the atmosphere.

The first part of the book provides some simple messages that cannot be ignored:

1) We need to do this now; it is not optional. We need to invest time and money right now to avoid a climate disaster that will have a considerably bigger economic and social impact than all previous post-war recessionary periods put together.

2) We have reached a position where we need to get carbon emissions to zero (or close to it) by 2050. Slow progress still leads to catastrophe. For example, a 50 per cent reduction in emissions from here would still lead to rising temperatures.

3) Our current reliance on fossil fuels makes the starting point of this structural shift very hard. Not only do we use fossil fuels in almost everything we do, from driving your car to brushing your teeth, they are also extremely cheap. Unless we commit to investing in zero carbon solutions, thereby reducing their costs, progress will be slow.

The next part of the book is a little more optimistic:

4) There are lots of potential solutions that we can apply in combination that would tackle carbon emissions across energy networks, transportation, agriculture and manufacturing.

5) Governments have become much more aligned in the last few years. The 2015 Paris Agreement was a big step forward. However, from here individual governments need to set policy that stimulates investment in the right areas in order to drive down costs.

6) Clear government policy reduces the risk for investors in key technologies and underpins investment growth.

7) A lot of the technologies are already cost effective for both the investor making a suitable return on their investment, and for the consumer, in terms of being able to pay for the end product. A positive cycle is created: the cost profile of these value chains only gets better as the end market size increases. Government policy can accelerate this trend.

8) Carbon taxes will need to be applied in a considered manner across developed markets versus emerging markets. They must be applied at industry level to encourage investment in clean areas, but also to consumers in order to encourage switching and drive demand.

The global energy system, when you combine electricity, transportation and heating/cooling, is effectively responsible for half of the 51 billion tons of greenhouse gases being released into the atmosphere. This change in the energy system to a more sustainable system is what people now refer to as the “energy transition”.

As investors in this trend, we are responsible for investing our clients’ money responsibly in the companies directly involved in the structural shift of the global energy system over the next 30 years.

The book really underlines some of messages that we have been conveying to clients. Here are six of the most important:

1. This structural shift in the energy system is a multi-decade investment phase: it is not cyclical, it is structural.

2. This investment phase has only just started and needs to accelerate from current levels to get anywhere close to net zero by 2050.

3. The amount of investment - estimated to be close to $100 trillion between 2020 and 2050 - is significant, both in terms of relative to previous energy investment cycles and relative to other industries.

4. Government policy is becoming ever more supportive and they will play a key role in incentivising investment, dis-incentivising areas of high emissions and driving down costs in key emerging technologies.

5. Costs within the energy transition value chain are already at a level in key technologies where they compete head on with fossil fuel alternatives. These costs will keep falling on a relative basis.

6. Consumers at both the commercial and residential level are increasingly shifting towards these end products, whether it is Microsoft only sourcing electricity from renewables or consumers buying electric cars. This trend will only accelerate over the next few years.

Long before he turned his attention to climate change and wrote this book, Gates had already articulated what can help in solving the seemingly unsolvable. And it has resonance for investors.

In 1996, he wrote: “We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten. Don’t let yourself be lulled into inaction.”

Mark Lacey is fund manager of the global energy transition fund at Schroders